The presidential election is right around the corner, and the S&P 500 and Dow Jones Industrial Average recently hit all-time highs. However, many Americans are nervous about this election’s impact on the markets, perhaps with memories of 2008 in focus.

While nobody can know what will happen for sure, historical data can help us navigate the perceived uncertainty surrounding the 2024 presidential election season. We have summarized key data points below.

Where We Have Been

Before we dive into historical data and trends, let’s consider where we have come from and how we have arrived in our current place.

S&P 500 yearly returns since 2016 are as follows:

2016: +9.54% (presidential election year)

2017: +19.42%

2018: -6.24%

2019: +28.88%

2020: +16.26% (presidential election year / Covid / can you believe it)

2021: +26.89%

2022: -19.44%

2023: +24.23%

2024: at the time of writing, the year-to-date return for the S&P 500 is +21.91% (this will change daily).

This is mentioned because it has been a wonderful time period to be a long-term investor. While we have experienced spats of volatility along the way, the long-term results have been quite favorable as we enter this election season.

Let’s also consider that, during this period, we got through COVID-19, the highest inflation in 40 years, rising interest rates, and plenty of geopolitical tensions.

Logic would dictate that a pullback of some kind could be in the cards in the future, but will the presidential election in and of itself be that catalyst?

Historical Election Year Returns & Volatility

While the S&P 500 historically has posted lower total returns in election years versus non-election years (data from 12/31/1927–12/31/2023), results have shown an average yearly gain of 11% and a median yearly gain of 14% during election years. Perhaps surprising — and not too shabby!

Historically, there has been a local spike in volatility in both equity and bond indices before and close to election days. We saw that in early October, with around 30 days until Election Day.

Of course, past performance is not indicative of future results, but historical data has its place in analysis.

October’s Reputation for Volatility

When it comes to presidential election years, there is a bit of a double whammy regarding volatility, as October tends to be the most volatile month of the year for stock markets.

Given the recent Fed rate cut, some interpretations are that it could be different this time. However, as October began, we saw volatility tick higher in the S&P 500, as measured by the VIX Index.

Post-Election Day: A Light at the End of the Volatility Tunnel?

Once traders and investors navigate through October and make it to November 5th, a dose of uncertainty becomes removed as a winner is declared.

We also see that, according to 90 years of data, volatility tends to fall sharply in December of election years, so there is always light at the end of the volatility tunnel. December also tends to be one of the better months of the year for stocks overall.

Election Outcome: Stocks or Bonds?

This question comes up a lot in financial circles, and there are varying interpretations surrounding the outcome of the election and what it could do for the financial markets.

Instead of trying to pick whether stocks or bonds are the better choices based on an election winner, having an appropriate blend of both types of assets for the long term is smart.

Election Season Mentality

There are all kinds of ways to think about what could happen during this election season and through the end of the year, and there is no shortage of opinions. Moreover, looking at historical data, there is no certainty that we can draw from.

But one thing is for certain: the long-term investing mentality should persist in our minds, regardless of election-related headlines (and there are sure to be many!).

Staying invested throughout market cycles includes presidential election cycles, and staying invested for the long term is what it’s all about.

With that said, please know that we are here as a resource for you if you have any financial questions or concerns this election season. Reach out anytime.

Take care,

Mosher Financial Advisors Management Team

Jerry S. Mosher, CFP® / Partner

Scott Dawson, CFP® / Partner

William Tom, CFP® / Partner

Jenny Giambastini, CRPC™ / Office Manager

Phone: 925-284-9470

Fax: 925-284-9492

Mosher Financial Advisors, LLC is a Registered Investment Advisor. Securities offered through American Investors Company, Member FINRA / SIPC

Research Highlights the Role of Employment in Divorce

By Scott Dawson, MS, CFP®

Money disagreements have been at or near the top of the list for reasons why marriages fail. While divorce rates have been dropping recently, 40 – 50% of marriages still end in divorce. There are many reasons why couples can’t make the relationship work, but money has been one of the main culprits.

I recently read an interesting article discussing a Harvard sociology professor and researcher, Alexandra Killewald, who found that the biggest factor leading to divorce is the husband’s job status. The study involved data on 6,300 married couples going as far back as the 1970s. The study showed that husbands who had been out of work for a long time had a higher chance of getting divorced than husbands who had stable employment. Men without jobs increased their odds of divorce by roughly 30%. The study found that the husband’s involuntary unemployment may negatively affect marriages more strongly than voluntary unemployment. The study results also indicate that women who were voluntarily or involuntarily unemployed didn’t have a significant risk for divorce.

One could conclude that the historical norm of the husband being the breadwinner still exists even though more women are working instead of staying at home with the kids. A stay-at-home husband’s risk of divorce may not be greater because it was a voluntary decision made by the family. The financial and emotional stresses that are caused by a husband’s inability to find full-time work and provide for the family seems to create more marital problems.

The study’s findings reinforced the importance of education, knowledge, and skills. Being employable is good for a couple’s financial well-being and marriage. Continuing to improve your skills and knowledge is a good practice in today’s ever changing economy and also in keeping a happy home life.

As you have probably heard, Equifax had a cybersecurity attack that potentially impacted 143 million Americans. The hackers accessed Equifax’s database from mid-May until July 2017 and they captured names, birth dates, addresses, social security numbers, and driver’s license numbers. In addition, 209,000 Americans may have had their credit card numbers accessed.

What steps do you need to take to see if you were affected? The first step is to check if you were one of the 143 million affected by the breach. You can visit Equifax’s website www.equifaxsecurity2017.com to determine if your information has been compromised. Once on the website, click Potential Impact and you will be prompted to enter your last name, and last 6 digits of your social security number, and then confirm you are not a robot. You will be told instantly whether you were impacted by the breach.

Because of the data breach, Equifax is offering one year free of credit monitoring to all Americans, which you can enroll for on the above mentioned website. Credit monitoring doesn’t prevent hackers from using your data, but helps you to monitor suspicious activity.

Whether you were impacted or not by the breach, it’s always a good practice to check your credit reports annually and look for unfamiliar or suspicious activity. Individuals are allowed to receive one free credit report every twelve months from each of the three credit reporting agencies: Equifax, TransUnion, and Experian. You can request your credit reports from www.annualcreditreport.com. In addition, always review your bank and credit card statements. Comb through each statement to ensure that you did make each purchase or initiated each transaction. Identity thieves sometimes start small and then go big.

If Equifax says your personal information has been compromised, you have a couple options: place a credit freeze or fraud alert on your credit files.

A credit freeze restricts access to your credit report, which means you or no one else can open new credit using your personal information. If you needed to make a purchase requiring a new application for credit, like a car loan or home refinance, you will be required to unfreeze your credit file. To initiate a freeze, contact all three credit reporting agencies by phone or internet. The cost to freeze and unfreeze your credit file varies by state. The cost usually is no more than $10 for each credit reporting agency, though Equifax is now waiving their fee.

Another option is a fraud alert. The fraud alert informs creditors that your identity may have been compromised and creditors will need to verify the identity of the individual trying to establish credit. To initiate a fraud alert, you can contact one of the three credit reporting agencies and the credit agency will alert the other two. Fraud alerts are available for 90 days or 7 years. A fraud alert for 7 years is only available to individuals who have been victims of identity theft and must provide documentation to the credit agencies. Otherwise, a fraud alert is only available for 90 days, but you can renew after it expires. There is no cost to place a fraud alert on your credit files.

To obtain more detailed information, visit the Equifax and Federal Trade Commission’s websites.

When I became a parent for the first time, I received a lot of advice from other parents. One piece of advice was to read to your baby. It didn’t matter what you read, I was told, just read something. Of course, I wanted to do the best for my daughter so I read to her every day. Being a working parent means my time is limited however, so instead of reading Dr. Seuss or children’s books, I read the Journal of Financial Planning, Money Magazine, Kiplinger’s, and financial articles that I either needed to read or wanted to read anyway. My hope was to catch up on my own reading, but in the process I might also plant the seeds that would eventually create a financially savvy daughter.

Fast forward five years and my oldest daughter just finished her first year of elementary school. It was a fantastic experience for her and us. School created so many memories and one in particular stands out for me.

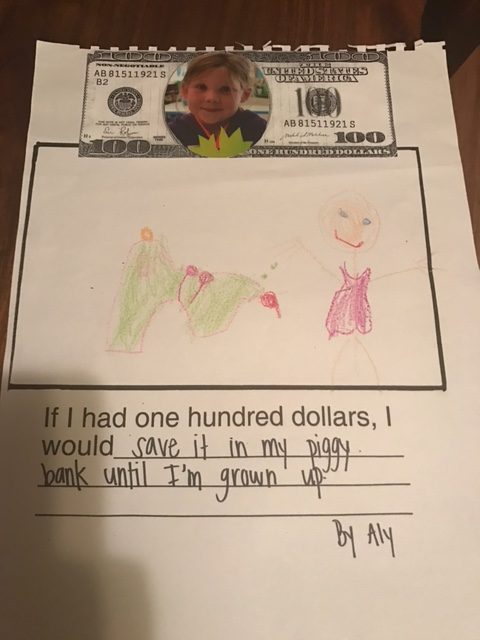

The teacher asked all the students in the class, “if I had $100, I would _____.” The teacher recorded all the responses and created a scrapbook with a picture of each student, the question, and the student’s answer. The scrapbook was sent home for each family to see. As my spouse and I were flipping through the scrapbook, we were reading all the cute responses from the students. Many responded as expected, using their $100 windfall to buy candy, dolls, or toys. Our daughter’s response was near the back of the scrapbook. As we got to her page, we saw it: “If I had $100, I would save it in my piggy bank until I’m grown up.”

Charitable giving is very personal. Individuals give in different ways based on their values and what they care about. Giving to many means writing a check or donating things, which I have done regularly through the years. There is another form of charitable giving that I have found to be very rewarding and has changed my life forever…donating my time.

Financial planning is something I value and care about and am pretty good at so I have donated my time sharing my knowledge for the sake of giving back to the community and helping others. Over the years, I have spoken to foster kids about financial literacy, given presentations on retirement, investment, and tax planning at libraries and a local college, coached financially struggling families for a year on various financial planning topics to help build better financial habits, volunteered for the Public Relations Committee, Scholarship Committee, Pro Bono Committee, and Board of Directors to chair the Pro Bono Committee for the Financial Planning Association’s East Bay Chapter. In each of these experiences, I felt like I made a difference in people’s lives, which was personally very satisfying.

The other day I overheard someone say, “Good things happen to people doing good things” and it resonated with me instantly. This quote is very meaningful to me because it reminds me how I met my spouse. Before I met her nearly 9 years ago, I signed up to participate in the most unlikely of places for singles…a pro bono financial planning event in Oakland. It was the East Bay Financial Planning Association’s first annual pro bono event and I donated my day to provide free financial planning advice to the public. Unfortunately, not many people showed up to share my financial wisdom. The number of financial planners outnumbered advice seekers by a good margin and there was lots of idle time. Fortunately, my spouse, who is also a financial planner, also decided to donate her time that day. Since we had no people to help, we got to know each other and talked about such riveting topics as safe withdrawal rates, investment philosophy, taxes, and retirement plans. What a blissful day it was!

Getting up that Saturday morning at 8am with the intent to help others was one of the best decisions I ever made. And now, two beautiful, healthy little girls later…my life has forever changed.

I regularly attend conferences and presentations about various financial planning topics. At a recent conference, I was reminded of some statistics about historical stock market declines in a given year. The stock market, on average, will have at least three 5% declines and one 10% decline in a year. Every three years, the stock market will decline by at least 20%.*

To put these declines into perspective, if an all equity investment account is valued at $500,000, a 5% decline is $25,000, 10% decline is $50,000, and 20% decline is $100,000. In 2008, the S&P 500 was down 37%, which is a $185,000 decline in our example.**

What does this mean?

Stock market declines are normal and expected. If the market goes down by 10% or even 20%, my thought is stocks are 10%-20% cheaper than they were. I’m a long term investor and I need to tolerate the fluctuations of the market to earn the higher rate of returns that stocks have historically offered above fixed income, which fluctuate much less.

No one can consistently predict when stock market declines will occur and how long they will last, but it’s comforting to know that declines have been temporary. Historically the stock market has always recovered. Maybe the next decline will be different, but history is on our side.

An approach to deal with the ups and downs of the stock market is to determine an asset allocation that allows you to stay the course. An asset allocation is the mix of stocks, bonds, and cash in your portfolio. It’s important that your asset allocation is based on your goals, risk tolerance, and time horizon. If normal stock fluctuations make you uncomfortable, then adding more fixed income will dampen the ups and downs of the market. Abandoning your investment strategy because of fear, the market going down, or greed, the market going up, has not been kind to investors’ long term financial health.

*Source: American Funds

**Source: Morningstar

All investing involves risk, including the loss of principal. Diversification and asset allocation do not guarantee a profit, nor do they eliminate the risk. Past performance is not indicative of future results. Investors should work with financial professionals to discuss their specific situation and investment goals

Did you know anyone can use the title financial planner and not all financial planners are certified? Only financial planners who have the CERTIFIED FINANCIAL PLANNER ™ or CFP® designation are actually certified. The CFP® certification is the gold standard in the industry and only planners who have fulfilled the certification requirements of the CFP Board can claim to be a CFP® professional.

To be a CFP® professional, a planner must abide and complete the four requirements known as the 4 E’s, which are Education, Examination, Experience, and Ethics.

Education

CFP® professionals must complete financial planning coursework through a college or university’s financial planning program as a prerequisite to taking the CFP® exam. The required coursework includes financial planning, insurance, retirement planning, employee benefits, investments, estate planning, and income taxes.

Examination

After completing all the financial planning coursework, the next step is taking the CFP® exam. The CFP® exam is a rigorous, comprehensive 6 hour exam covering the financial planning coursework with case studies and questions to ensure that the planner has the knowledge and is highly qualified to help a client with their finances.

Experience

In additional to completing the education and exam components, CFP® professionals must have at least three years of financial planning-related experience. This ensures the planner has real life practical client experience with the theoretical knowledge from their coursework to help clients develop a financial plan based on their individual needs.

Ethics

CFP® professionals are also held to the Standards of Professional Conduct as outlined by the CFP Board. Planners are obliged to uphold the principles of integrity, objectivity, competence, fairness, confidentially, professionalism and diligence as outlined in CFP’s Code of Ethics. The Rules of Conduct require CFP® professionals to act in the best interest of their clients. The CFP Board has the right to revoke the use of the CFP® certification for the violation of these standards.

To maintain the CFP® certification, a planner must complete 30 hours of continuing education every two years, which includes 2 hours of ethics. This is critical to keep up with the ongoing changes in the industry.

When looking for a financial planner or advisor, I always recommend confirming that your planner has the CFP® certification.

Each year the IRS announces the annual contribution limits for retirement savings accounts.

For 2017, the IRS announced that there will be no change in the annual contribution amount for 401(k), 403(b), 457 plans, and IRA.

The annual limit for employees contributing to 401(k), 403(b), and 457 plans will remain at $18,000 for individuals under age 50 and $24,000 for those 50 or older.

The annual contribution limit for Traditional and Roth IRA will remain at $5,500 for individuals under 50 and $6,500 for those 50 or older.

The annual limit for employees contributing to a SIMPLE IRA will remain at $12,500 for individuals under 50 and $15,500 for those 50 or older.

For more detailed information on any of these changes, please visit the IRS website.

Mangoes are relatively new in my life. My mother never bought them. My friends never ate them and so it wasn’t until I was first exposed to mangoes on a surf trip with my brother to Ecuador in 2008. On that trip, I had my first taste and ate one every day and also ordered fresh mango drinks, which consisted of pureed mango and water, with meals. My brother commented, at one point near the end of the trip, “another mango!” Ever since that trip, my brother has consistently given me a mango for my birthday or Christmas.

As I eat my lunch today, which includes a mango, I was thinking about how the spending decisions we make every day affect our finances. As a consumer, I am very aware of what I purchase. I do my best to purchase things that I value, but am very cost conscious as well. I was raised to save a portion of what I earned and spend no more than needed.

Besides valuing mangoes, I also value eating well with cost in mind. For example, I bring my lunch to work almost every day. A typical lunch consists of a peanut butter sandwich on wheat bread, fruit, and tap water. I love my lunches. They are healthy, tasty, and low cost. The alternative would be to eat out for lunch every day. I could pick up a burrito, sushi, or Thai, but it will definitely cost me a lot more than my typical lunch. My typical lunch probably costs $2 and takeout would cost me anywhere from $7-10. The additional savings does add up over the year. A $5-8/day lunch savings, based on 240 working days, amounts to $1,200-1,900/year. Would eating lunch out on a regularly basis bring me enough joy to justify the extra $1,200-1,900 difference. To some, the answer is yes, but to me it doesn’t. I would rather spend the extra savings on a vacation, which is an experience rather a material item, for example. Studies have shown that experiences bring us much more happiness than material things. I have found this to be true for me.

This is one example of how I think and spend on things I care about without feeling like I’m depriving myself or sacrificing my pleasure. I really don’t feel like I’m missing out by bringing my lunch. Everyone is unique and believe there are opportunities to examine what we truly care about and take action to reduce spending on things that we might not value and reallocate those savings to things that you really do care about and value. For me I bring my lunch to work, for you, it is ________?

Should you pay for your children’s college education?

By Scott Dawson, MS, CFP®

The question that many parents grapple with is whether they should pay for their children’s college education. The answer is not clear cut. Many parents feel it’s an obligation and will sacrifice their own retirement security. If you have looked into college expenses, public universities cost about $30,000 year and private universities about $60,000 including room and board. The cost of one year of public university is more than my first year salary out of college. Ouch!

Here’s my college story and maybe it will have you consider other options than picking up the entire bill for your child’s education.

I was the oldest child in my family and the first to go to college. When I was exploring colleges, my parents told me that they couldn’t afford to pay for four years of college for my brother, sister, and me. Their offer was to pay for my tuition and books at a public university or junior college. The cost of room and board would be at my expense, or if I wanted to live at home I could live room and board free. It was an appealing offer since I had worked since the age of 14 and knew the value of a dollar. Up to that point, the most I had ever made in a year was a few thousand dollars. At the time I was applying for college, tuition and books were about $500 a year at the local junior college and $2,000 at public universities. The cost of room and board was estimated at $10,000 year. The cost of room and board was multiple times more than I had earned in an entire year. I knew that paying for this from part-time employment would be challenging.

Also, I was raised to avoid debt and I knew that if I wanted to live on campus that I would have to incur debt, which didn’t make me feel comfortable. On the other side, after growing up in the Bay Area, I did like the idea of going to school in San Diego, living on the beach, and surfing daily. For those who don’t know me, one of my passions was surfing. I started surfing when I was 12 and had been getting rides to local San Francisco beaches and eventually driving myself when I received my license once I turned 16.

The choice my parents allowed me to decide was clear: was going to school in San Diego vs staying local worth the expense of taking a student loan? It was a major decision for a 17 year old to make but a valuable one. The choice was all mine and I was forced to explore my values. I had to think about all alternatives. Was an education in San Diego vs San Francisco area worth the extra cost to me? I had lots of friends in the area. I got along very well with my parents and siblings. My existing good life as I experienced it would continue. I had a good life and I had no desire to leave the home except for the lifestyle I thought I wanted to lead on the sunny beach in San Diego. Was the appeal to pack up and start new with a new experiences and friends worth the trade-offs that I had to make?

I finally concluded to stay local and bypass San Diego. I attended the local junior college for two years, even though I was accepted to multiple universities, and transferred to San Francisco State University a couple years later. I lived with my parents during my college years and enjoyed it. I continued to surf with my friends. As I think about it in hindsight, the decision was a win-win for everyone. My parents paid about $6,000 for my undergraduate degree, which was a bargain, and experienced another 4 years of time with me. I graduated from college debt free and since I worked while in college, my net worth actually increased. As I read about the student loan debt saddling recent college graduates, I value my choice even more.